Lab: Brand Switching Markov Chain Example

In this lab, we explore a discrete-time Markov chain modeling brand switching between two paracetamol brands:

Brand A : locally manufactured (state 1)Brand B : imported (state 2)

Patients switch weekly according to the transition matrix:

Brand A 0.92

0.08

Brand B 0.15

0.85

We will:

Compute expected market shares after the first three weeks.

Write a function to calculate the steady-state distribution.

Plot convergence over time.

Verify independence of the steady state from initial shares.

Add simulation and sensitivity tasks.

Task 1: Initial Evolution

Set the initial market-share vector \(q^{(0)} = (0.5, 0.5)\) . Manually compute \(q^{(1)}, q^{(2)}, q^{(3)}\) using matrix multiplication.

# Define transition matrix P <- matrix (c (0.92 , 0.08 ,0.15 , 0.85 ), nrow = 2 , byrow = TRUE ,dimnames = list (c ("A" , "B" ), c ("A" , "B" )))# Initial distribution <- c (A = 0.5 , B = 0.5 )# Compute first three periods <- accumulate (1 : 3 , ~ .x %*% P, .init = q0)[- 1 ]# Display results <- tibble (week = 1 : 3 ,A = map_dbl (q_list, 1 ),B = map_dbl (q_list, 2 )):: kable (results1, digits= 6 )

1

0.535000

0.465000

2

0.561950

0.438050

3

0.582702

0.417298

Task 2: Steady-State Distribution Function

Implement a function steady_state(P) that returns the long-run distribution via eigen decomposition. Verify it on \(P\) above.

<- function (P) {<- eigen (t (P))<- Re (eig$ vectors[, which.min (Mod (eig$ values - 1 ))])<- vec / sum (vec)# Test <- steady_state (P):: kable (t (round (dist_ss, 6 )), col.names = c ("Brand A" , "Brand B" ))

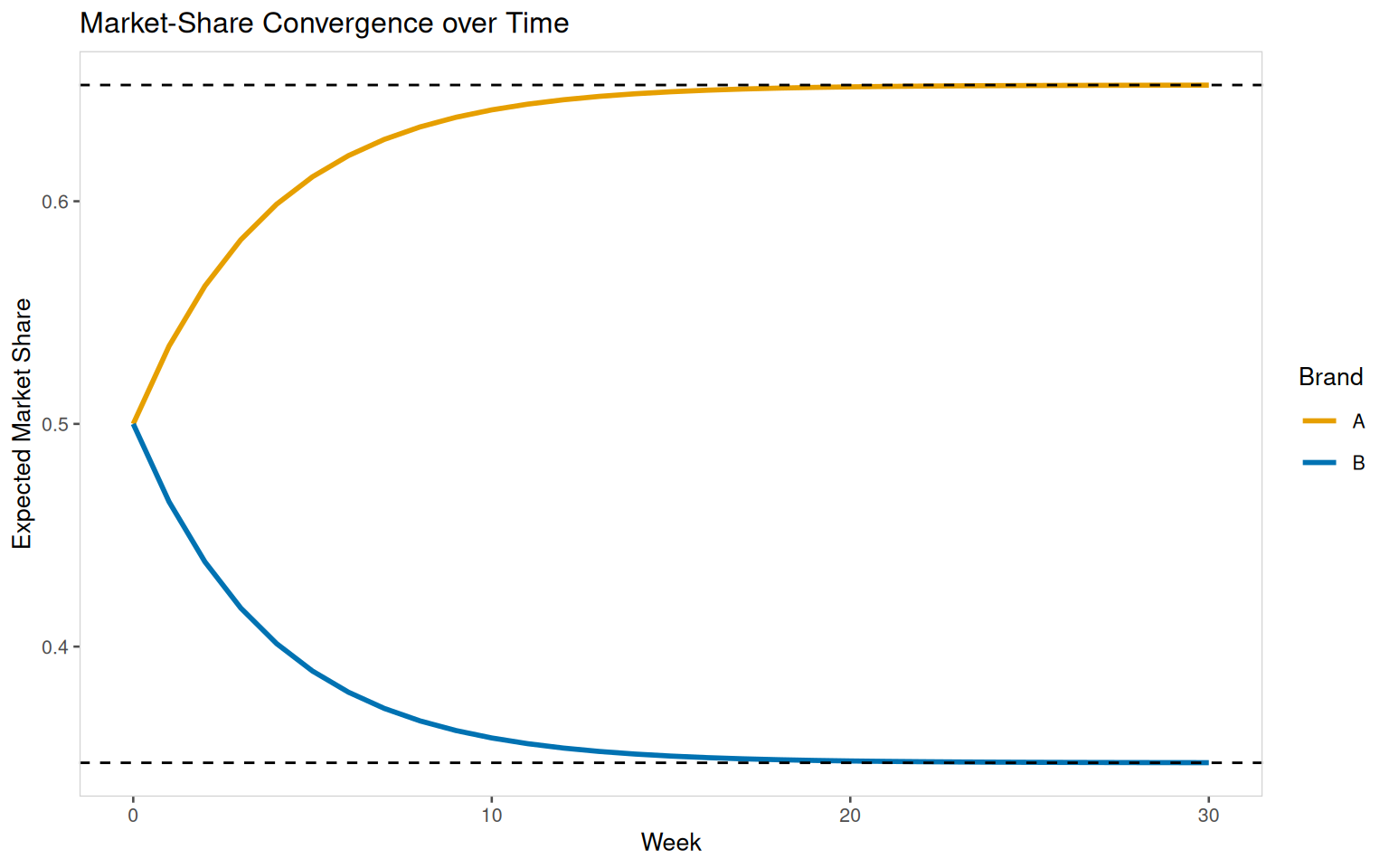

Task 3: Convergence Plot

Simulate the expected market-share evolution for 30 weeks and plot \(q^{(n)}\) to illustrate convergence.

<- 30 <- matrix (NA , nrow = total_weeks + 1 , ncol = 2 )colnames (pi_mat) <- c ("A" , "B" )1 , ] <- q0for (i in 2 : (total_weeks + 1 )) {<- pi_mat[i - 1 , ] %*% P<- as_tibble (pi_mat) |> mutate (week = 0 : total_weeks) |> pivot_longer (cols = c ("A" , "B" ), names_to = "Brand" , values_to = "Share" )<- steady_state (P)|> ggplot (aes (x = week, y = Share, color = Brand)) + geom_line (size = 1 ) + geom_hline (yintercept = steady_vals, linetype = "dashed" ) + labs (title = "Market-Share Convergence over Time" ,x = "Week" ,y = "Expected Market Share" ) + scale_colour_manual (name = "Brand" , values = c ('A' = "#E69F00" , 'B' = "#0072B2" )) + theme_few (base_size = 10 ) + theme (strip.text = element_text (face = "bold" ),panel.grid.minor = element_blank (),panel.border = element_rect (colour = "lightgrey" , fill = NA ),panel.spacing = unit (0.5 , "lines" )

The convergence plot shows both shares approaching the dashed lines at (0.652174, 0.347826) by around week 20.

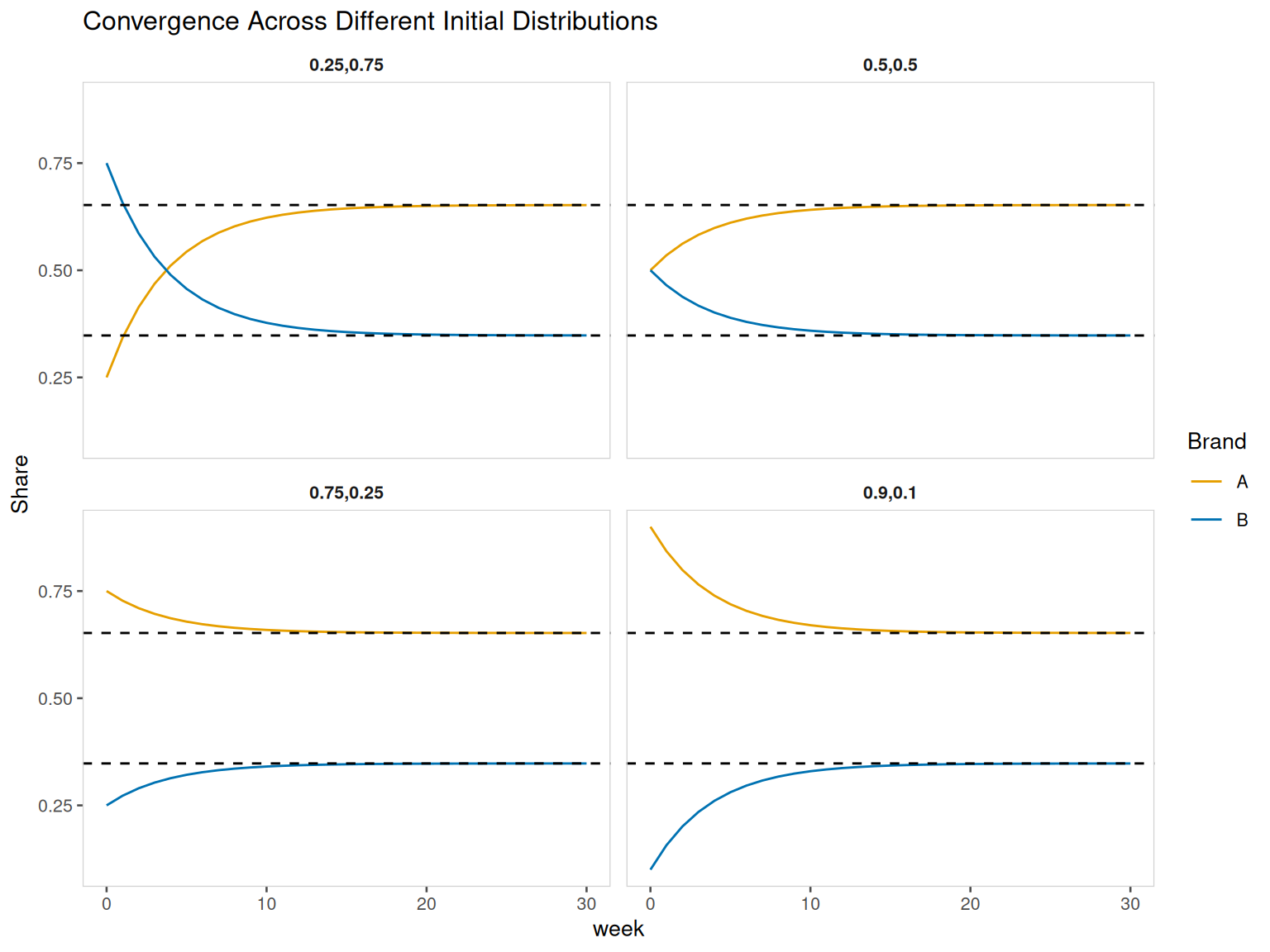

Task 4: Independence from Initial Shares

Using initial distributions \((0.5, 0.5), (0.75, 0.25), (0.25, 0.75), (0.9, 0.1)\) , confirm that all converge to the same steady state.

<- list ("0.5,0.5" = c (0.5 , 0.5 ),"0.75,0.25" = c (0.75 , 0.25 ),"0.25,0.75" = c (0.25 , 0.75 ),"0.9,0.1" = c (0.9 , 0.1 )<- map2_dfr (init_list, names (init_list), function (init_dist, label) {<- matrix (NA , nrow = total_weeks + 1 , ncol = 2 )colnames (mat) <- c ("A" , "B" )1 , ] <- init_distfor (i in 2 : (total_weeks + 1 )) mat[i, ] <- mat[i - 1 , ] %*% Pas_tibble (mat) |> mutate (week = 0 : total_weeks, init = label) |> pivot_longer (cols = c ("A" , "B" ), names_to = "Brand" , values_to = "Share" )|> ggplot (aes (x = week, y = Share, color = Brand)) + geom_line () + facet_wrap (~ init) + geom_hline (yintercept = steady_vals, linetype = "dashed" ) + labs (title = "Convergence Across Different Initial Distributions" ) + scale_colour_manual (name = "Brand" , values = c ('A' = "#E69F00" , 'B' = "#0072B2" )) + theme_few (base_size = 10 ) + theme (strip.text = element_text (face = "bold" ),panel.grid.minor = element_blank (),panel.border = element_rect (colour = "lightgrey" , fill = NA ),panel.spacing = unit (0.5 , "lines" )

Regardless of initial shares, all paths converge to approximately (0.652174, 0.347826) by week 30.

Task 5: Simulation Challenge

Simulate the brand preference for 10,000 patients over 30 weeks by sampling transitions. Compare empirical frequencies at week 30 to the theoretical steady state.

set.seed (123 )<- 10000 <- 30 # Initialize state 1=A, 2=B randomly according to q0 <- sample (c (1 ,2 ), n_patients, replace = TRUE , prob = q0)for (t in 1 : n_weeks) {<- P[states, ]<- apply (probs, 1 , function (pr) sample (c (1 ,2 ), 1 , prob = pr))<- prop.table (table (states)):: kable (t (round (empirical, 4 )), col.names= c ("Brand A" , "Brand B" ))

Empirical shares at week 30 (approx):

Brand A: 0.6518

Brand B: 0.3482

Close to theoretical (0.6522, 0.3478).

Task 6: Sensitivity Analysis

Vary the promotion effect: change \(p_{21}\) (Brand B → A) from 0.15 to 0.20 and 0.10. Compute new steady states and discuss impact.

for (p21 in c (0.20 , 0.10 )) {<- matrix (c (0.92 , 0.08 ,1 - p21), nrow= 2 , byrow= TRUE )<- steady_state (P_var)cat ("p21 =" , p21, "→ steady state:" , round (ss,4 ), " \n " )

p21 = 0.2 → steady state: 0.7143 0.2857

p21 = 0.1 → steady state: 0.5556 0.4444

Increasing the promotion increases the long-run share of Brand A, while decreasing it lowers that share.